Tax Planning Techniques for Real Estate Investors

The “Like Kind Exchange”

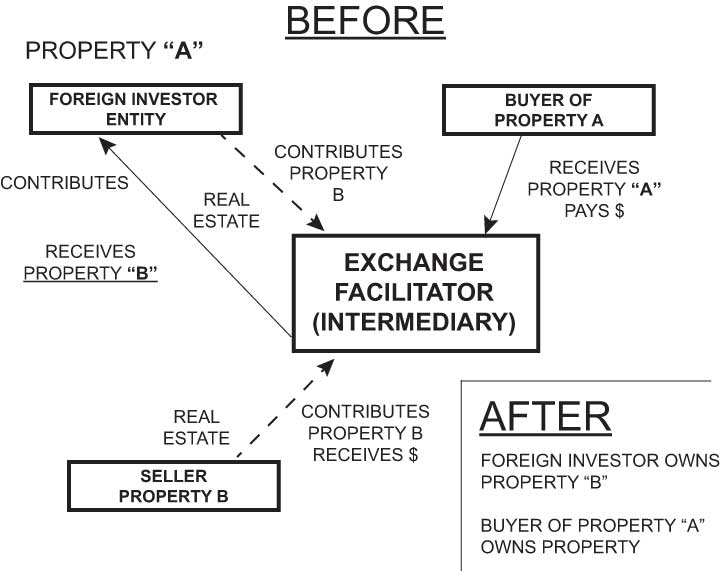

Real estate investors whose property increased in value may change their investment from one real estate investment to a different real estate investment of a higher value without paying tax on the gain in their original asset until a later point in time.

A taxpayer may invest in a real estate property, (property), and not sell but may exchange that real estate property; which has increased in value for a completely different type of real estate property, equal to the increased value of the second property, without paying tax on the gain represented by the increased value of the new property until a later date in time when the property no. 2 is actually sold by the foreign investor.

The tax on the gain is deferred until that time the asset is actually sold to a third party.

- This is accomplished by insuring that the new appreciated asset will continue to be owned at the old reduced cost or basis of the property asset that has been exchanged.

Code Section 1031 governs Like Kind Exchanges

- The exchange property be identified “on or before the day which is 45 days after the date on which the taxpayer transfers the property relinquished in the exchange” is an arbitrary cutoff date which must be strictly complied with.

- The exchange property must be received on or before the earlier of ;

- the day which is 180 days after the date on which the taxpayer transfers the property relinquished in the exchange or

- the due date (including extensions) for the transferor’s return for the taxable year in which the transfer of the relinquished property occurs.

Identification of Multiple Properties

The maximum number of replacement properties that the taxpayer may identify is

- three properties without regard to their fair market values or

- any number of properties as long as their aggregate fair market value as of the end of the identification period does not exceed 200% of the aggregate fair market value of all of the relinquished properties as of the date the relinquished properties were transferred by the taxpayer.

In the case of replacement property that is to be produced, the fair market value for purposes of the 200% rule is its estimated fair market value as of the date it is expected to be received by the taxpayer.

Like-Kind Exchange Survey from the National Association of REALTORS