Taxation of the Clawback in a Ponzi Scheme

This article unfolds in an interesting fashion. Every item we cover in this article is a building block to the next item – until we come to the last portion of the presentation when it will all fit together.

Any lawyer involved in a clawback settlement agreement must, where possible, in the settlement agreement, distinguish between and earmark the two types of clawback that can happen. There can be a clawback of profits earned from the ponzi scheme or a clawback of invested principal.

As you will see there is a distinctly different tax treatment between the two clawbacks and as a general rule, clawbacks allocated to profit losses may be more valuable for larger refunds but also may be more treacherous to deal with.

One cannot understand the taxation of the clawback in a ponzi scheme without first understanding how a direct ponzi scheme loss is treated under the tax law.

The “direct ponzi scheme” loss is the loss that occurs when the scheme explodes and nothing is left as opposed to the loss that results from clawback payments. These are payments made after the Ponzi scheme becomes a bankrupt estate.

The taxpayer must also learn about what is called the “mitigation section”.

This is internal revenue code section 1341 that permits one type of the clawback payment to be taken as an ordinary income deduction in the year in which the clawback income was originally taxed even if the year is closed by the statute of limitations; while another type of claw back payment may be deductible only in the year of payment.

The taxpayer needs to know how to deal with “tax losses” from the clawback payment and how those losses can best be used, either to receive a refund from taxes paid in the past; or a “carry forward” of those losses to offset future income.

When all of this is put together you will see how effective the mitigation provision can be.

We will start with a summary of the basics.

The tax analysis of losses in a ponzi scheme and ultimately the Ponzi scheme clawback losses starts with the deduction in the internal revenue code for theft losses. In particular to the Ponzi scheme it is code section 165(c)(2). That code section states:

There shall be allowed as a deduction any loss sustained during the taxable year and not compensated for by insurance or otherwise.

Limitation on losses of individuals

In the case of an individual, the [loss] deduction . . . Shall be limited to losses incurred in any transaction entered into for profit . . .

There are several IRS publications that are helpful in understanding the law of ponzi scheme losses and the clawbacks of ponzi scheme profits and principal. We will discuss them during the seminar. For a review of the basics, we will just discuss the most important, findings of those publications.

First the IRS considers a loss in a ponzi scheme as a theft loss.

Theft definition

A theft loss is any type of taking that is considered a theft under state law, and that’s a very broad definition.

A definition from one of the cases reads ;

“For federal income tax purposes, theft is a word of general and broad connotation covering any criminal appropriation of another’s property to the use of the taker, including theft by swindling, false pretenses and any other form of guile. A taxpayer claiming a theft loss must prove that the loss resulted from the taking of property that was illegal under the law of the jurisdiction in which it occurred, and was done with criminal intent. However, a taxpayer need not show a conviction or theft or even the bringing of an action”.

Taxation of Clawbacks

What you see in this presentation is that we must go building block – by building block – for you to understand fully the last portion of this presentation that pulls all of this together and shows how to maximize the tax value of clawback losses.

We now come to the principle of clawbacks and the taxation of the funds paid in a clawback.

What happens in ponzi schemes, is that certain parties either intentionally or unintentionally actually may make out very well in a ponzi scheme. They may receive all of their money back before the scheme explodes or may have received a profit that was distributed in cash, and never lost in the scheme.

The trustee of a ponzi scheme in bankruptcy obtains a clawback and that money is put back in the pot for the other Ponzi scheme victims.

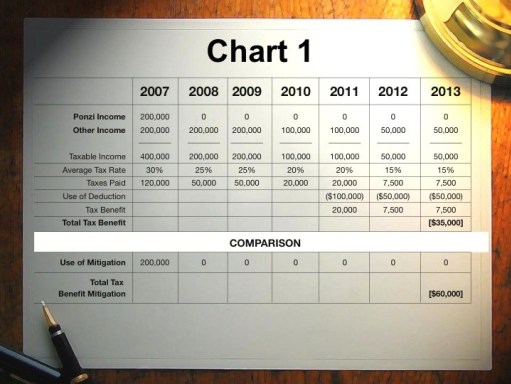

CHART 1 is a comparison: Deduction of clawback vs Exclusion of clawback

First, we will discuss CHART I. You will understand it much better at the end of the seminar. However, it graphically shows the tax effects of the right way versus the wrong way. The effects are dramatic and will focus your attention to this technical and valuable tool.

In this chart you will see a comparison from a single example, how different the end result can be. The chart compares the cash refund of a deduction versus the refund from the mitigation section under circumstances in which a Ponzi scheme profit of $200,000 was earned in 2007 in addition to the Taxpayer’s Other Income and the clawback occurred in 2013. A deduction and its carrybacks versus relying on the mitigation section is almost one-half as valuable as the amount of the mitigation refund.

A clawback can come many years after, and what will typically happen in a clawback is, after a taxpayer has paid the clawback, there is a deduction for the money paid to make the clawback payment in the year of payment. That deduction can reduce the taxes in the year of the deduction and excess losses can be used to apply for a tax refund of prior taxes for a two-year period or the deduction can be carried forward to be used against future income for twenty years.

After the dust has settled for all of the direct ponzi scheme victims, and years later, the clawback target may not be making a lot of taxable income because they too may have lost money in the scheme.

Therefore, the tax benefit from paying the clawback funds could amount to very little if it is deducted in the year it is repaid. If one is in the 15% tax bracket in the year the clawback is paid, they are only going to get 15 cents on the dollar back as a refund. They might have paid taxes on that same income to the U.S. and the state in which they reside equal to 40% of the income.

Mitigation

We are going to thoroughly explore how to get out of this trap.

If you have made a clawback payment, what you will see is that you can get out of the trap in two different ways, depending upon (1) whether the clawback is a clawback of previous reported profits or (2) the clawback requires a payback of an investor’s principal investment to the trustee.

There is a particular section in the internal revenue code (the ‘mitigation section’) that would allow you to deduct clawed back funds that represent profits from the year in which those funds were paid to the investor and taxed.

That is typically going to be high earning years. If you qualify, the mitigation section may provide you with a much larger tax refunds.

We are going to study a unique Internal Revenue Code section that permits the clawback victim to actually be in a better position than those who lost funds directly in the ponzi.

Since the mitigation section is complicated we are going to look at each of the elements that must be met if one is to benefit from it and why a Ponzi scheme clawback meets those definitions.

One has to understand this code section to appreciate how valuable it is.

Facts

As you see in Chart 2 – The Tax Rate was 30%.

For the taxable year 2008, a corporate taxpayer reporting income on the calendar year basis had taxable income of $20,000 on which the taxpayer paid a tax of $6,000.

Included in gross income for such year was $100,000 received under a claim of right as royalties, the tax rates are calculated at 30%. For each of its taxable years 2005, 2006, 2007, 2009, 2010, and 2011, the corporation had taxable income of $10,000 on which it paid tax of $3,000 for each year.

In 2012, the corporation returns the entire amount of $100,000 of the royalties earned in 2008. In 2012 the corporation has taxable income of $25,000 for a tax of $7,500 (without taking the deduction of $100,000 into account). If the deduction is taken in year 2012, no tax is paid for 2012 and there is a net operating loss of $75,000 (taking the deduction of $100,000 into account).

The net operating loss of $75,000 for 2012 (taking into account the deduction of $100,000) is carried back under the net operating loss rules, 2 years. Taxable years (2010 and 2011) in the manner shown.

The entire taxable income for those years is eliminated by the carryback, and the corporation would be entitled to a refund of the tax for such years in the aggregate amount of $13,500 with total deduction(s) used of $45,000. The remaining $55,000 of the net operating loss for 2012 would be available as a carryover to taxable years after the taxable year 2012.

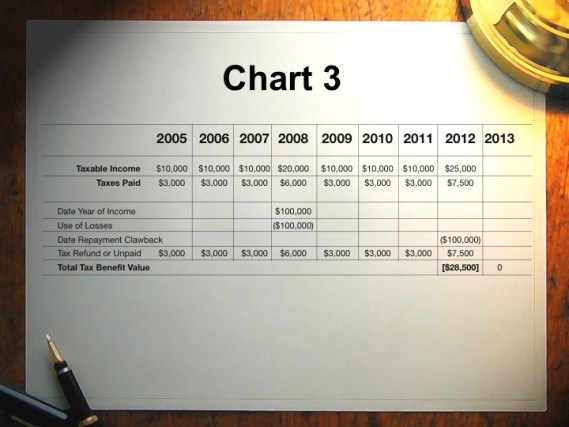

In Chart 3, as an alternative, under the mitigation section the taxpayer will deduct nothing in 2012 but will exclude $7500 from gross income for the taxable year 2008 (the year in which the item was originally included).

This results in a net operating loss of $80,000 for such year ($20,000 taxable income minus the $100,000 exclusion), thus decreasing the tax for 2008 year by the entire amount of $6,000 paid.

The resulting net operating loss of $80,000 for 2008 is available as a carryback to 2005, 2006 and 2007 and as a carryover to 2009, 2010, 2011, and 2012. Since the aggregate taxable income for these taxable years is $80,000, only $20,000 of the 2012 taxable income of $25,000, is eliminated by carryback and carryover.

This leaves tax on such remaining $5,000 of taxable income for 2012 is $1,500, thus decreasing the tax determined for such year by $6,000, ($7,500 minus $1,500).

Under section 1341 the decrease in tax for the prior taxable years exceeds the tax for the taxable year of restoration computed without the deduction of the amount of the restoration by $16,500. However, there are no additional losses carried forward

One must see why care must be taken when the mitigation section is relied to make sure that the losses that are being carried back and carried forward do not exceed all of other income that can be offset prior to the payment date as those excess losses cannot be carried forward.

If the mitigation section is used, since the computation results in an available refund of only $13,500 for the taxable years to which the net operating loss for 2012 is carried back, and since the mitigation computation results in an overpayment of $28,500, it is determined that the mitigation section applies.

Accordingly, the $28,500 is treated as having been paid on the last day prescribed by law for the payment of tax for 2012 and is available as a refund.

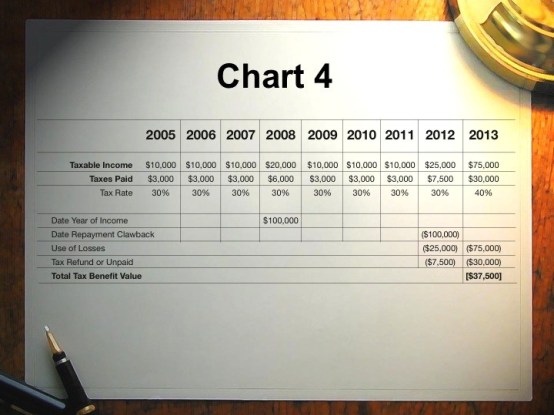

In today’s world we need to go even a step further and look at the alternative that becomes relevant when taxes are higher.

Finally (chart 4) we have assumed we are in the present day and that the tax rates after the clawback payment have moved up to 40%; when the loss in the year of payment and the loss carry forward might have a tax value of $37,500.

In this CHART 4 it is assumed that the taxpayer lives in a state with a state income tax, a city with a city income tax and the average tax rate is 40% between the three taxes. At that point the best choice is clearly, take the deduction in 2012. Do not carry back losses (which is an election), but carry losses forward of $75,000 for the future years will result in $37,500 in cash refunds or taxes avoided.

One can see there is potential to lose tremendous amount of money with loss carrybacks and loss carry forwards that can’t be used if it is not done right.

In the income tax situation, just the year of discovery is going to make a difference in when people can get their money, how the taxpayer can get their money, whether they get their money back at the highest tax brackets.

You need to know all of your options. That’s the heart of the tax planning. You need to have your crew of professionals so that you can scope out in numbers and hard dollars every option that you’ve got and be able to choose the best ones that have the quickest legal answers and the best financial answers for you.

The mitigation section

We have seen the refund differences by using the mitigation section of the case. Internal revenue code section 1341, (the mitigation section); was designed to allow someone who pays funds back in a clawback to be able to go back to the year that the Clawback income was earned for tax purposes and exclude that income to calculate which tax result would be more valuable. This permits the taxpayer to use the clawback; in the year in which the highest tax bracket and tax value is found.

Since this is a beneficial section for the taxpayer, the IRS is strict about making sure one qualifies for who this was intended to help.

We are going to study the mitigation section carefully to see how the Ponzi scheme clawback fits in this mitigation section.

The claim of right doctrine

The study of the mitigation section starts with “the claim of right doctrine”.

This tax doctrine states that if a taxpayer receives income in a particular year, but was forced to repay it in another year, the taxpayer cannot go back to the original year and correct the original year in which the income was earned. The original year most often was closed by the statute of limitations and it was impossible to unwind the statute of limitations.

This led to terrible inequities such as you saw in the example. The mitigation section was passed to cure this inequity.

This section has several requirements to achieve this equity and has intricate rules dealing with the loss carry back and carry forwards in the mitigation section. These need much care, or else valuable deductions can be lost.

We are going to take a good look at the “mitigation section” requirements.

The ponzi clawback meets each and every one of these requirements. As I said, we still study them as part of building blocks to appreciate the end result.

The mitigation section has four important requirements and one requirement that is outdated by now. They are:

- An item of income must have been included in a prior taxable year.

- Because it appeared that the taxpayer had unrestricted right to that item of income.

- The taxpayer must be able to claim that in the year that the clawback was made, a deduction would be allowed for the payment.

- The fourth important requirement is that it must be established after the close of the prior taxable year that the taxpayer did not have an unrestricted right to the income that was refunded.

- The fifth requirement is that the amount of the deduction must exceed $3,000.

Item included in gross income

What we’re going to do now is explore each one of the first four important items and consider them in some detail.

The first item required for mitigation is that an item of income must have been included in gross income for a prior taxable year or years.

The word “item” is defined in the law. In the internal revenue code, there is a definition of the word item of gross income, and certain specific items are listed. However, that definition is not limited just to the specific items listed. The word “income” includes all income from whatever source it is derived.

Guidance as to what is an “item” of gross income is found in code section 61.

That code section provides a specific definition for gross income and a general one. The income ‘items’ that might be used in a ponzi could include any of the following types of fraudulent income payments.

The code section defines income as: “Except as otherwise provided . . .. Gross income means all income from whatever source derived, including (but not limited to) the following items”.

- Compensation for services, including fees, commissions, fringe benefits, and similar items;

- Gross income derived from business;

- Gains derived from dealings in property;

- Interest;

- Rents;

- Royalties;

- Dividends;

- Annuities;

- Alimony and separate maintenance payments;

- Income from life insurance and endowment contracts;

- Distributive share of partnership gross income;

- Income in respect of a decedent; and

- Income from an interest in an estate or trust

It is clear ponzi schemes can be built around any of the items.

Inventory

It is very important to keep in mind that the inventory of a taxpayer’s business or transaction entered into for profit is accounted for under its own unique set of tax principals and is not within the mitigation provisions.

Apparent, unrestricted right to such item

The next qualification that the taxpayer seeking mitigation must have is the “apparent right to the income” that the taxpayer reported in the prior year. What is the law after here?

Essentially, the legislation is designed to make sure that (1) no one can “voluntarily” use the mitigation section and (2) that income subject to mitigation was subject to the taxpayer’s unrestricted right at the time of reporting.

The mitigation section does not apply unless the taxpayer included the item in gross income in a previous year because it appeared that the taxpayer had an unrestricted right to the income. The taxpayer must have some right to the income but need not have an unchallengeable right in the year of inclusion.

The mitigation section does not apply if the taxpayer included the income item because he or she had an absolute right and must make the repayment for reasons other than a determination that no right existed to the income initially reported.

However, at least one court has stated that an apparent right to income may exist because a taxpayer reports an item as taxable income in a tax return, holding that a prima facie case is made that the taxpayer believed the income was the taxpayer’s. The court stated:

“Since [the taxpayer] took into income the item, it is clear that [the taxpayer] believed that it had a right to that income.”

The reasoning of the court is important here because the court stressed that since the mitigation provision is remedial it should be interpreted in favor of the taxpayer.

Certainly in the case of the Ponzi scheme, every objective indication is that there is an apparent right to income that is being reported by that investor. The ‘clawed back’ income is reported on the investor’s tax return, was available for distribution to investors until the crash came and, was in fact distributed to many investors. As can be seen by the many lives devastated by ponzi scheme perpetrators, the funds were counted on by all ponzi investors as real and critically important to their lives.

The claim of wrong exception to the claim of right principal

Equally important to eliminating the potential to manipulate the mitigation section was the idea that a “mitigation provision” in the law should not be available to wrongdoers.

To be entitled to mitigation, a taxpayer must not only have had an apparent right to the reported income; the taxpayer must have not wrongfully obtained that income. This means that if the taxpayer had no right at all to the income when it was received, the taxpayer could not receive mitigation treatment when later if that same income had to be refunded.

Thus the mitigation section does not apply to certainly wrongly claimed rights to funds. For example, the repayment of embezzled funds because embezzled funds may be included in gross income but there is no valid claim of right. Mitigation requires an unrestricted claim of right by the taxpayer.

The IRS position is that a taxpayer cannot have any right to income and therefore claim mitigation for its repayment, if the original income was “wrongfully obtained.”

This doctrine has been applied in cases of embezzlement, smuggling, kickbacks, and ill-gotten gains and rarely in a civil fraud setting. One thing has been clear. The “claim of wrong doctrine” cannot exist in a civil situation where there is no intentional wrongdoing such as a clawback victim.

The claim of wrong exception could not apply to the typical Ponzi scheme victim. This is a taxpayer who loaned or invested money with a highly respected and presumably trustworthy and wealthy member of the community (who turned out to be a con man). This clawback payer is a victim, not a wrongdoer.

Nonetheless, every settlement agreement should include statements about the clawback victim’s innocence and non-involvement in the Ponzi scheme.

Entitlement to deduction in year of payment

The third requirement is that the actual year of payment when the taxpayer pays the clawback, the payment must be a permitted deduction in that payment year.

Simply put, it means that clawback paid in the year 2012, for example, must be deductible in that year under a particular code section. Once that standard of deduction has been met, if the clawback represents a payment of profits earned in a prior year, the mitigation section will be available.

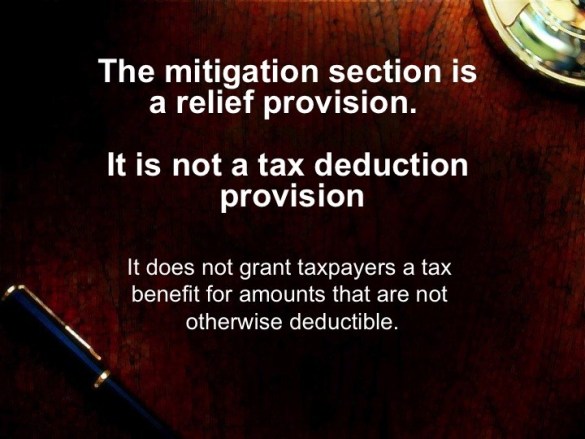

The mitigation section is a relief provision. It is not a tax deduction provision. It does not grant taxpayers a tax benefit for amounts that are not otherwise deductible.

Relationship between deduction and inclusion

Not only must there be a “deduction” in the year of payment, the relationship between the “deduction’ and the clawback payments are critical.

Clawback losses are not lost directly in the Ponzi scheme. Clawback losses are a repayment that was paid as profits or it is a payment of principal that was previously repaid to the Ponzi scheme investor.

The purpose was, quite simply, to ensure that, when the taxpayer found itself to be the losing party in the dispute and had to turn over specific funds to the rightful owner, the taxpayer should be able to re-compute its income for the year of receipt so as to entirely reverse the tax liability due to the disputed item.

What the courts have tried to do is make sure that if one is going to use the mitigation section and get a deduction for an item paid in a later year, there must be a close relationship between the item of gross income that’s originally recorded and the item of gross income that is being refunded and for which a deduction has been claimed.

In short, where the later payment arises from a different commercial relationship or obligation, and thus is not a counterpart or complement of the item of income originally received, the same circumstances test precludes application of section.

One court’s statement about this doctrine is helpful.

“The requirement that there be a nexus is inherent in the concept of “restoration” itself”.

A few examples from the case law also describe the necessary nexus of the repayment. The tax court has held that mitigation was not available for an executor’s reimbursement of an estate’s late filing penalty because the reimbursement was not a repayment of the commissions previously included in the investor’s gross income. The court ruled that the penalty would have been required even if no commissions had been received.

In another example, it was held that a doctor who had benefited from false insurance claims made by the professional corporation that paid the doctor’s salary was not entitled to use the mitigation section because the false claims had generated income for the professional corporation and not for the doctor, explaining that the item originally included in income was the doctor’s salary, whereas the restitution payments derived from the fraudulent insurance claims were submitted by the corporation.

A great number of cases have found that obligations that arose to remedy environmental damages did not demonstrate the restoration of an item of income to an entity from whom the income was received or to whom the item of income should have been paid.

These cases have been helpful in defining the substantive nexus between the right to the income at the time of receipt and the subsequent circumstances necessitating a refund.

Many cases in the environmental field have made the point that a company’s environmental cost, or “new obligations” of cleaning up waste did not arise from the same circumstances terms and conditions as the initial failure to spend additional funds to prevent waste.

Rather the obligations were created by new circumstances terms and conditions, namely, by an intervening change in environmental legislation.

The Ponzi Scheme Clawback – Same Circumstances

It would seem that the “same circumstances” test is generally going to be satisfied on the very face of the Ponzi clawback transaction. Had it not been for the Ponzi scheme investment, there would be no tax on, or reporting and payment of, the income that is returned in a clawback. The Ponzi investment and the clawback are directly related to each other from the same circumstances. The clawbacks repayment certainly seems to be a direct result of the same circumstances and the same Ponzi scheme that caused the clawback victim to report income in the first place.

However, as we will see the Internal Revenue Service does not believe the clawback of profits is deductible as a theft loss. Instead, the service provides almost identical treatment to these clawbacks as ordinary loss deductions because they are “non theft investment losses”.

Either way, whether the loss is a “theft loss” or a non theft investment loss, the IRS has considered it is an ordinary loss. The taxpayer is satisfied either way.

Repayment because lack of unrestricted right established

If the taxpayer in the past should have never included the funds in income or if the taxpayer included the income under an absolute right and makes the repayment for reasons other than a determination that no right existed the mitigation section will not apply.

In other words, the taxpayer’s repayment must be involuntary.

The fourth requirement of the mitigation section is that income that must be restored to another person because it was established after the close of a prior taxable year (or years) is not income which the taxpayer had an unrestricted right to such item (or portion thereof).

In other words, it must be clear that the taxpayer did not voluntarily return funds in order to profit from the mitigation provisions. There was a good deal of litigation on just what was meant by the “established” requirement.

The courts clarified this significantly.

The bottom line is that the best proof of this will be a good faith settlement agreement reached with the clawback trustee.

A judicial determination adverse to the taxpayer is not a prerequisite to a conclusion that the repayment is involuntary, but the repayment must arise out of a determination that any claim pursued against the taxpayer would be resolved adversely to the taxpayer.

This part of the code section is mainly trying to distinguish between taxpayers that appear to have a legitimate right to unrestricted right to gross income, and pay the tax on it; and taxpayers who really had no actual right to the gross income that they may have reported in prior years.

Examples of this are:

In the fourth requirement, the statute requires that when the taxpayer refunded the clawback monies, it must be clear that the taxpayer did not voluntarily return funds in order to profit from the mitigation provisions.

One case states that the “established” requirement is met under the following circumstances:

The general rule is that a good faith, non collusive settlement agreement entered into to terminate litigation will “establish” a liability to return income, thereby establishing a lack of an unrestricted right to income for purposes of section 1341.

A taxpayer’s good faith efforts in the Ponzi scheme to resist repayments of money in a fraud should meet the requirement of the law.

This concept of 1341 is best understood by analyzing two landmark cases that at the same time had decided both this issue and the standard that must be met for a deduction under the “established” requirement. Some courts interpreted the Barret case and the Pike case as being in contradiction about this “doctrine of voluntary payment”.

In Barrett, the taxpayer had included profit from the sale of stock options in one year and then, in a later year, the securities and exchange commission brought administrative proceedings against the taxpayer on the basis of alleged insider trading.

The taxpayer settled the case without admitting liability and claimed that the settlement payment deserved section 1341 treatment. Barrett held that a settlement that was made at arm’s length and in good faith could satisfy the “establishment” requirement of section 1341, stating:

The source of the obligation [to repay] need not be a court judgment; however, there must be a clear showing . . . Of the taxpayer’s liability to repay.

In contrast to Barrett was the Pike case, which involved a taxpayer who bought and sold corporate stock in one year, after which an investigator found that the profit from said stock should have gone in the corporation and not the taxpayer. The taxpayer then paid the money to the corporation, without admitting that the profits belonged to the corporation, and avoiding controversy so that he did not suffer harm to his professional career.

The Pike court stated that, although “a judicial determination of liability is not required . . . It is necessary under section 1341 for a taxpayer to demonstrate at least the probable validity of the adverse claim to the funds repaid.”

Although the holding in Pike and Barrett are different due to distinguishable facts, the point of law that they stand for is not. The primary distinction is that in Pike there was no suit against the plaintiff for repayment of money, which makes it more likely that the taxpayer acted voluntarily in paying the money and less likely that the taxpayer can “demonstrate at least the probable validity of the adverse claim.” Voluntary restitution will not meet the establishment requirements.

In Barrett, an actual settlement was made with the plaintiff(s) who had filed a suit, the taxpayer denied liability when entering into the settlement, and there was no indication that the settlement was not made at arm’s length. Under these circumstances, the taxpayer has met the establishment test. This is going to be the typical scenario in a clawback situation.

The amount of the deduction must exceed $3,000

The last requirement might give you some idea of how long this section has been in the code. The minimum amount of actual tax revenue at stake, about $500.00; to bring mitigation claim is about a six months tab at Starbucks.

Summary – The clawback of Profits

So, the Ponzi scheme clawback of profits passes all of the tests of the mitigation section.

The perpetrators promise extrordinary returns in almost every one of the many types of listed income “items”. The taxpayer believes he or she has the right to take the item into income and does so, paying tax on the income.

The year in which the taxpayer pays the clawback will be a year in which the taxpayer will receive a deduction for the repayment and the successful trustee in a clawback will have established there was no right to the income.

The compliance with the $3,000 deduction minimum goes without saying.

One more bit of background before we proceed with how the “ponzi theft loss” deduction and the “mitigation section” are married together to provide the best of all worlds; we are going to review a little history in this area.

In the year 2008 the Madoff ponzi scheme erupted and the IRS was swamped with cries for professional guidance on how to deal with Madoff victims’ losses. The tax law of financial thefts was unsettled and confusing at the time and the IRS published two extremely helpful documents in 2009 that greatly clarified matters. These consisted of Revenue Ruling 2009-9 which spelled out the law of deductions for ponzi scheme losses and Revenue Procedure 2009-20 which provided an easy administrative path for injured taxpayers to recover the taxes paid on their lost funds if they met certain standards and had clear evidence of a criminal ponzi scheme loss.

Neither of these publications directly commented on the deduction of a clawback. However the earlier rulings did specifically prevent direct ponzi losses from using the mitigation section. This made sense because in direct ponzi losses, there is no “repayment” of income earned from a prior year.

There was also a revenue procedure that outlined an easy administrative process to claim refunds from direct ponzi losses only. This was called the safe harbor. We are going to talk very little about the “safe harbor” the safe harbor is very meaningful for direct Ponzi scheme victims but not for the clawback.

These publications said very little about the clawback. They did completely clarify the law on direct ponzi losses.

In clearing up a lot of the confusion, the revenue ruling came to several legal conclusions about direct Ponzi scheme losses. But, the revenue ruling and the 2009 revenue procedure both considered principally the question of how to deduct the victim’s direct losses of ponzi scheme phantom profits upon which taxes had been paid and the amount of the principal lost in the investment. The revenue ruling opined on the following about these losses.

The Law on Direct Ponzi Losses was Clear.

-

Theft loss deductions. The revenue ruling defined the word “theft” for tax purposes and held that a ponzi scheme loss was a theft loss that resulted from a “transaction entered into for profit”. It was not a capital loss.

-

Ordinary loss. The revenue ruling clarified the benefits of a business oriented theft loss. The ponzi scheme loss is an ordinary deduction for losses incurred in a transaction entered into for profits.

-

Deduction is not subject to certain limitations on its use. As an ordinary loss, the ponzi theft loss is not subject to the limits on personal deductions or the limits on itemized deductions.

-

Deductible in year of discovery. The theft loss is deductible in the year the loss is discovered.

-

Amount of theft loss in a ponzi scheme.

Keep in mind this is not the standard being used in a clawback to determine amounts. The service also defined the amount of the loss that was available for the theft loss deduction by Ponzi scheme victims.

However, it is here that the definition of loss changes, since there is no “phantom income” lost in the clawback.

Loss carries over and carries back.

The last critically important IRS advice is that operating losses, arising from a theft loss, could be carried forward 20 year and carried back for 3 years. This is different from the typical loss carryback from a transaction entered into for profit or a business deduction, which is 2 years. In arriving at this conclusion the IRS also ruled that the ponzi victim’s investment was like a sole “proprietorship” and was entitled to the loss carryback as such.

The revenue ruling only considered direct losses from ponzi schemes where no additional payments were required. This is not the taxpayer’s case in a Ponzi scheme Clawback. In a Clawback situation, the losses come after the Ponzi scheme has failed and they are a result of a forced repayment, not an original payment.

The revenue ruling and the revenue procedure also considered effects of the tax law on claw backs. However, neither document presented the full picture of the deductibility of “claw backs” since the main focus of both documents was on the treatment of victims of immediate direct losses suffered when the ponzi scheme was first discovered and the investment funds and phantom profits were found to be worthless and nonexistent.

Nevertheless, even the revenue ruling implies that a clawback may very well be distinguishable from a direct theft loss that is unable to use the mitigation section because there is no “restoration of funds” in a ponzi scheme loss.

However, the revenue procedure and the revenue ruling did not give any direct IRS position or answers to the tax treatment of clawbacks.

The IRS F.A.Q.

Three years after the publication of the revenue ruling and the revenue procedure, in late 2012, as more and more clawbacks began to surface, the IRS provided some guidance for the taxation of clawbacks in a publication by the IRS entitled “frequently asked questions (F.A.Q.)”, related to ponzi scenarios for clawback treatment”.

The information was posed as two questions and answers.

Question: How does a taxpayer treat the repayment of a clawback?

Answer: Clawback repayments of amounts previously reported as income from a ponzi scheme are not additional theft loss deductions. Instead, they are repayments of claim of right income that result in either a deduction as a non theft investment loss, or a credit calculated under [the mitigation section] whichever results in lower tax.

A theft loss deduction from a ponzi scheme is not a deemed repayment of ponzi income that is eligible for the mitigation section . . . however, an actual clawback repayment is not a theft loss deduction and section 1341 treatment is not barred.

[The mitigation] . . .applies and the taxpayer would compute the tax for the year of the clawback payment (the clawback year) under two methods:

The F.A.Q. Then proceeded to show how to do the alternative calculations to use the claw back of profits either as a deduction in the year of payment or exclusion in the year the clawed back income was earned.

Method 1: figure the tax for the clawback year claiming a non-theft investment loss deduction for the clawback payment. It is not a capital loss and it is not subject to the 2% floor on miscellaneous itemized deductions.

Method 2: figure the tax for the clawback year with a credit computed as follows:

- Figure the tax for the clawback year without deducting the repaid amount.

- Refigure the tax for the year the clawed back income was originally reported (the income year) without including in income the amount of the clawback payment.

- Subtract the hypothetical tax for the income year in (2) from the actual tax shown on the return for the income year. This is the section 1341 credit.

- Subtract the answer in (3) from the tax for the clawback year figured without the deduction (step 1).

The taxpayer is entitled to the benefit of either the deduction under method 1 or the credit under method 2, whichever results in less tax (or a greater refund) for the clawback year. Note that the section 1341 credit is a refundable credit.

The second question asked and answered in the F.A.Q. :

Question: What does the taxpayer need to establish as to whether the repayment of a clawback is allowable as a deduction (or a section 1341 credit)?

Answer: usually a settlement agreement will have been entered into. The taxpayer has to establish that the clawback amount was required to be repaid to the trustee. The taxpayer would also have to substantiate that payment was made. The substantiation could include a letter from the trustee.

Clawback of the Principal of a Ponzi Scheme Investment

In the F.A.Q. The IRS provided more concrete guidance on clawbacks. However, again it was not complete guidance as it was directed at only one aspect of the clawback.

The F.A.Q. Considered only the tax treatment of the clawback of Ponzi scheme profits (“profits”), upon which taxes have been paid. Though the F.A.Q at first glance appears to encompass all clawback tax treatments, it in fact does not consider the treatment of the clawback of an investor’s principal investment.

The first paragraph of the F.A.Q. Directly states that the F.A.Q. Is dealing with “repayments of amounts previously reported as income from a ponzi scheme”.

These are profits earned by that after the fact must be repaid; to be shared by victims of the same scheme. The profits returned in a clawback are deductible as ordinary losses incurred in a transaction entered into for profit, but not as theft losses. According to the F.A.Q.

However, they do make it clear that though clawback repayments of amounts previously reported as income from a ponzi scheme are not additional theft loss deductions. Instead, they are repayments of claim of right income that result in either a deduction as a non-theft investment loss, or a credit, whichever results in lower tax.

Clawback of profits – theft loss or transaction entered into for profits losses

It would seem that the clawback of ponzi scheme profits would be deductible as repayments of previously reported income from a ponzi scheme that are treated as theft loss deductions. However, this is not the theory adopted by the Internal Revenue Service.

The F.A.Q. permits the taxpayer to have an ordinary deduction that is available for clawbacks of profits; but not as a “theft loss”. Rather the loss is permitted under what is in effect the theory that the loss is from a “transaction entered into for profit”. 2

The F.A.Q. uses the term “non theft investment loss” to describe the ordinary loss resulting from a clawback of profits. That term is not found in any tax library or on Google other than the reference in the F.A.Q.

The treatment of Clawback of invested capital (principal) withdrawn from a ponzi scheme

The F.A.Q does not deal directly with a clawback payment that pays to the trustee any original principal paid in to the ponzi scheme and has been withdrawn from the scheme.

This clawback payment represents the investor’s principal investment that is lost at a later point in time than the discovery of the theft. However, it is nevertheless lost due to a ponzi scheme theft. It is not a repayment of anything. It represents principal funds, that had they not been withdrawn and remained in the Ponzi scheme, would have been lost with the rest of the victims.

The F.A.Q. directly relates only to the clawback of ponzi scheme income. However, often a settlement may include a substantial portion of the clawback that represents the loss of investor principal.

The F.A.Q. Did not publish any materials on the tax treatment of the clawback of principal.

As a practical matter, any settlement agreement that is being reached in a ponzi scheme should include language to clarify the item being clawed back, the amount of the clawback and other tax issues. Tax counsel prior to finalization should review settlement agreements involving a clawback.

Though nothing has been published, the service has considered the issue of the treatment of a clawback that results in a taxpayer’s loss of the investor’s principal investment in the ponzi scheme.

Now is when our knowledge of the theft loss must again come back into play.

Late in may I spoke with an attorney with the chief counsel’s office of IRS he was very familiar with the F.A.Q. and advised me in no uncertain terms that the service position was to treat ponzi scheme principal losses that result from a clawback, in the same manner as the principal losses suffered by original investors. (i.e., those victims who invested principal and lost their principal funds when the Ponzi scheme was bankrupted).

This in fact means that IRS position is to permit the loss of principal in a ponzi scheme as a theft loss whether it is paid directly or as a result of a clawback.

Several aspects of the law support the IRS position. The IRS has confirmed in its revenue ruling 2009-9 that investors in ponzi schemes are engaged in a “transaction entered into for profit” and entitled to “sole proprietorship” treatment for purposes of the net operating loss rules under code section 172.

The F.A.Q. ruled that the Clawback of income was entitled to be treated as a loss resulting from the transaction and the IRS has ruled that the loss of principal is unlike the loss of profits because there is no “repayment of income”, such as we had in the claw back of profits.

Therefore, the principal lost in a Clawback is not entitled to use the mitigation section for its losses.

Certainly, there is a loss as a result of a clawback of principal. This loss of principal, whether it be lost as part of the direct ponzi scheme loss or whether it be lost as a result of a clawback that forces the taxpayer to replace principal previously withdrawn, are both treated identically. Losses are both incurred directly as a result of investing in a ponzi scheme. Ponzi losses of principal and profits are both treated as ordinary losses.

Time of discovery – the theft loss and the clawback of principal

Furthermore, the theft loss of principal resulting from a clawback is not “discovered” until it was paid in full. Since certainly there will not be a “recovery” of any of the clawback, and the principal is deductible as a theft loss, it should be that the entire amount of the theft loss (or 100% of the lost principal is deductible).

Because the theft loss resulting from a ponzi scheme is permitted as an ordinary loss, the taxpayer is permitted to use the rules that permit deductions for net operating loss carry overs and carry backs to the year of the payment.

Summation

Under certain circumstances there may be more tax value in a section of the internal revenue code that corrects an injustice in the tax law. This injustice occurs if the profits being returned in the clawback are deducted in a year when they were of little value because the tax rates were low in the year of payment; and yet the income that is paid back was earned in a year in which the taxes were high.

However, this injustice is corrected only as to a loss of profit that must be paid back. They do not apply to losses of principal.

The tax value of clawed back profits may be calculated as the higher of the tax value of the deduction in the year the Clawback is paid or the value of the deduction if one assumes that the profits that were repaid as a result of the clawback; should never have been taxed in the year they were taxed in the first place.

Consequently, when dealing with clawbacks, it is important to keep the different characteristics of the two clawbacks clear and then make the most use of those separate characteristics.

1.) Profits

(a) The clawback of profits is not a theft loss. It is an ordinary loss from a transaction entered into for profit, and the losses of which can be carried back for two years and forward for twenty (20) years as a general rule.

(b) The value of this clawback is entitled to be calculated under tax rules that maximize the clawback’s tax value whether (i) it was deductible in the year it was paid; or (ii) excluded as income in the year it was first considered as taxable income.

2.) Principal

(a) The claw back of principal is deductible as a theft loss. It is an ordinary loss, deductible only in the year of discovery. It will have a three (3) year loss carryback and twenty (20) years carry forward.

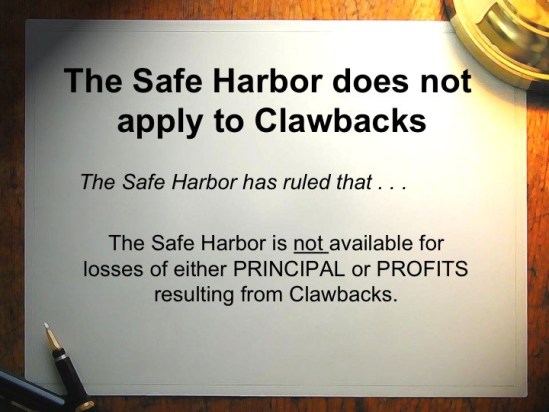

The Safe Harbor and the Clawback

The second document published by the IRS, known as the “safe harbor” for Ponzi scheme losses was revenue procedure 2009-20. This in fact is an administrative procedure that the IRS undertook in order to make sure that those ponzi schemes that could be clearly described as having violated state or federal criminal laws would have a “fast track” system with the IRS for administrative approval of claimed losses.

The safe harbor has strict standards and requires taxpayers to waive certain rights. In those cases where a Ponzi scheme perpetrator does fit in the safe harbor, the loss from that particular Ponzi scheme may be deducted directly with little interference at the administrative level. However, in the first year of loss, the taxpayer agrees to deduct only 95% of the total loss.

The safe harbor has ruled that the safe harbor is not available for losses of either principal or profits resulting from clawbacks. Since this is an administrative ruling the IRS can write the rules and one must comply exactly or the administrative grace of the safe harbor does not apply.

The net operating loss rules

The net operating loss rules become very important in mitigation. Especially in clawbacks.

One must know the tax situation of the ponzi clawback victim for many years in the past. Mitigation is not quite as simple as it seems, for a taxpayer to reap the most value from the clawback. This is because the mitigation section allows the taxpayer to go back to the year the clawed back profits were earned and then carryback losses from that original year to previous years for purposes of a claim for refund.

Net operating losses arising in year of repayment

A special rule applies for a deduction of an item is repaid in a year that generates a net operating loss for that year.

- First, the net operating loss is carried back under the normal net operating loss rules, which is usually for a period of two (2) years.

- Second, the alternative decrease in tax is computed under the mitigation section.

- The amount of decrease in tax liability for those prior taxable years caused by the net operating loss carryback is computed.

If the amount computed under the first step exceeds the amount computed under the second step, the taxpayer treats any remaining net operating loss in the usual manner.

If the mitigation section is applied, a deduction is not taken in the year of payment for any of the repaid funds; other than as a result of a loss carry forward resulting from the mitigation calculation.

Adjustments to a liability of previous year

In recomposing the tax liability for the year in which the income item was included under the claim of right doctrine, the taxpayer must take into account any redeterminations, deficiencies, credits, and refunds attributable to that year, in addition to the tax liability shown on the return for that previous year.

In recomposing the tax liability for the taxable year in which the income item was included under the claim of right doctrine, the taxpayer must adjust those items whose computation depends on the amount of gross income or adjusted gross income, such as charitable contribution deductions under section 170, casualty loss deductions under section 165(h), medical expense deductions under section 213, miscellaneous itemized deduction limitations under section 67, itemized deduction reductions under section 68 and similar items.

Net operating loss arising in previous year of inclusion

A special rule applies if reducing gross income for the previous year in which the income item was included under the claim of right doctrine generates a net operating loss for that year. The net operating loss for the previous year is carried back under the usual rules, and the decrease in tax is not only the decrease in tax for the previous year of inclusion but also for all the other previous years to which the resulting net operating loss is carried. Any remaining Net Operating Loss is carried forward under the usual rules.

Now we are going to turn to our Chart 1 with a much better understanding of all of those amounts and understand how certain losses can be taken to maximize cash refunds to clawback victims as opposed to loss carry forwards.

Summary

The summary starts by going back to one of the original charts. Now we will look at the chart 1 and study it more carefully.

It is extremely important that all of taxpayer’s clawback losses from the ponzi scheme (the “ponzi scheme”), be accounted for. In order to maximize the value of deductions. This includes all of the income or “profit” paid upon which the taxpayer has paid taxes (the “profit”) and the principal invested for the year of the deduction in the ponzi scheme (the “principal”). For purposes of filing the year. We will need to differentiate precisely between what is a loss of principal and what is a repayment of profits.

It is important to note that the IRS has made a distinction between losses of a clawback that is considered to be a “repayment” of profits earned in a ponzi scheme; and losses that result from invested principal that is lost as a result of a ponzi scheme clawback.

The typical victim in a ponzi scheme can have a loss of both principal and a loss of reported profits that were “reinvested” in the Ponzi scheme and never distributed to the ponzi victim, (“phantom income”). The victim for tax purposes has reported this phantom income and taxes were paid.

The direct loss in a ponzi scheme of phantom income and invested principal are both considered to be an ordinary income loss that resulted from the theft that had occurred in a transaction entered into for profit. This results in an ordinary income deduction.

This is the manner in which Ponzi scheme tax recovery works for direct losses by ponzi victims who lost their funds when it was discovered the Ponzi scheme went bad.

However, the deduction for the Clawbacks does not follow this exact pattern. Clawbacks, that require a successful investor to pay back profits, upon which taxes have been paid, are not treated as theft loss deductions by the IRS nevertheless these clawbacks are treated as ordinary losses. On the other hand, a clawback of principal is considered a theft loss deduction from a transaction entered into for profit.

A clawback of profits is treated as a “repayment” of funds that result in an ordinary loss because the ponzi scheme is a transaction entered into for profit. However, they are not considered theft losses.

The clawback of profits is treated as an ordinary loss because of the fact that investing in a Ponzi scheme means an investor has lost their profits in a “business like” investment suffered by a sole proprietor. Those losses are still treated as an ordinary loss but not considered to be theft losses.

On the other hand, the amount of the principal investment in the ponzi scheme, that has been clawed back, is not a “repayment of income”. A principal payment made in a clawback is considered the same as a direct loss of the principal lost in a ponzi scheme.

Consequently, the loss of principal in the ponzi investment as a result of a clawback receives the same theft loss treatment that is available to direct losses of principal in the ponzi scheme.

Either way, the service seems to have come to the opinion that both types of clawback losses are considered to be ordinary losses.

However, the distinction is important in terms of the loss carry back rules. Those rules differ between the two types of ordinary loss. The business loss has a two (2) year carry back period while the theft loss carry back period extends for three (3) years.

In the event that there were significant taxable earnings in 2008 from the ponzi scheme, this may become important.

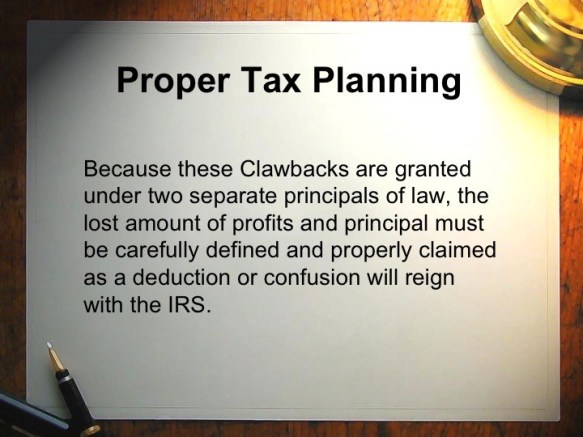

Because these clawbacks are granted under two separate principals of law, the lost amount of profits and principal must be carefully defined and properly claimed as a deduction or confusion will reign with the IRS. Thank you.

Footnotes:

-

references to “direct ponzi losses” refer to the ponzi loss suffered when the investor first discovers the fraud and bankruptcy of the scheme. Clawbacks refer only to payments made to the trustee in repayment of profits for the forfeiture of the principal investment as part of the Clawback.

-

as a practical matter, any settlement agreement that is being reached in a ponzi scheme should include language to clarify the item being clawed back, the amount of the claw back and other tax issues. Tax counsel prior to finalization should review settlement agreements involving a Clawback.

This topic qualifies for CLE accredited tax law credits for Florida Attorneys.

Mr. Lehman believes in sharing his knowledge to those who are interested in the complex topic of United States taxation. These CLE credits are offered at no cost and are available on-demand to all who would like to learn more. All seminars are Florida Bar Accredited.

- Taxation of the Clawback in a Ponzi Scheme – Maximum Tax Recovery (2 CLE Credits)

Total presentation time: 01:32:07

Level: Intermediate

View this presentation and resources here.