![]() Richard S. Lehman, Esq.

Richard S. Lehman, Esq.

ATTORNEY AT LAW

2000 Glades Road, Suite 312, Boca Raton, FL. 33431 • Tel: 561-368-1113

CONTACT ONLINE

Mr. Lehman believes in sharing his knowledge to those who are interested in the complex topic of United States taxation.These videos and resources are free to everyone.

These videos and articles cover a complete range of topics dealing with legal and practical advice for foreign investors that invest in United States businesses, United States real estate and United States securities; and aliens that immigrate to the United States. This includes income, estate and gift tax planning for nonresident alien individuals and foreign entities such as foreign corporations, foreign trusts and foreign partnerships. Special sections are devoted to foreign investors in United States Real Estate, Tax Planning and Pre-Immigration Tax Planning.

Pre-Immigration Income Tax Planning

An immigrant coming to America for longer than a certain time period will become a Resident Alien for U.S. income taxes at some point in time. In doing so, they are subjecting themselves to a potential U.S. tax income on their annual worldwide income, an estate tax on their deaths on their worldwide assets and a tax on gifts of their worldwide wealth.

Below is a short 6-minute video segment on pre immigration tax planning:

The below video is on the topic: Tax Planning Techniques for the Foreign Real Estate Investor (Advanced) Presented by Richard S. Lehman, Esq.

Tax Planning for Foreign Investors Acquiring Larger (One Million Dollars and over) United States Real Estate Investments

Today the Foreign Investor has the time to think about making your purchase and it need not be hurried but one cannot wait for all of the signs of correction before committing. The U.S. real estate market is very depressed. At the same time the U.S. real estate market will not be depressed forever and may turn quickly when it turns. click here to read full article

Tax Planning for Foreign Investors Acquiring Smaller ($500,000 and under)

United States Real Estate Investments

This is an article about tax planning for the non resident alien individual and foreign corporate investor that is planning for smaller size investments in United States real estate -- "The Foreign Investor" click here to read full article

U.S. Taxation of Foreign Investors

The following narrative outline below, by Richard S. Lehman Esq., is intended to provide the foreign investor, both corporate and individual, with a basic introduction to the tax laws of the United States as they apply to that foreign investor.

Download entire outline in these languages:

English | French | German | Italian

Spanish | Chinese | Arabic | Russian

By Richard S. Lehman Esq.

1. U.S. Taxation of Foreign Corporations And Nonresident Aliens General Rules

2. Tax Planning Before Immigrating to the U.S.

3. Tax Planning for the Foreign Real Estate Investor

INTRODUCTION

The United States has long been a safe haven for foreign investors. Now it has become not only a safe haven for foreign investors, it has also become a nation that has myriad real estate and business assets all available for acquisition at bargain prices due to the precipitous fall in the U.S. dollar.

What is not so well known is that the United States tax laws are very favorable to foreign investment; providing at times for the payment of tax free interest by U.S. taxpayers to foreign investors. Capital gains from investment may be tax free or subject to tax rates of 15%, and the complex laws provide for numerous methods of deferring the payment of U.S. taxes to a later point in time.

At the same time, these same laws can become tax traps for the poorly advised investor and can cause income taxes on profits to be as high as 65% and estate (inheritance) taxes to be paid on U.S. assets held at death as high as 48%.

The following narrative outline is intended to provide the foreign investor, both corporate and individual, with only a basic introduction to the tax laws of the United States as they apply to that foreign investor. Hopefully, it will let the foreign investor know that they are welcome in the United States. More importantly, it should help the foreign investor know that the U.S. tax laws are complex and must be dealt with in a highly professional manner; if one is to avoid the tax traps and take advantage of the many tax benefits offered by the United States.

The general principles discussed herein are not intended to be legal or tax advice and taxpayers should consult with their individual legal, accounting, and tax advisors.

U.S. Taxation of Foreign Investors Table of Contents

III. TWO TYPES OF FEDERAL INCOME TAXATION PATTERNS

IV. THE EFFECT OF BILATERAL TREATIES

VI. PRE-IMMIGRATION PLANNING – INCOME TAX AND GAINS

VII. PRE-IMMIGRATION PLANNING – ESTATE AND GIFT TAX

VIII. EXCEPTIONAL CIRCUMSTANCES AND SPECIAL TAX BENEFITS

IX. REAL ESTATE - TAXATION PATTERN

XI. TAX PLANNING BENEFITS AND TRAPS UNIQUE TO THE FOREIGN INVESTOR IN REAL ESTATE

I. TAXATION PATTERN

- United States Resident Alien ("Tax Resident") - Subject to Taxation

a. Income Taxation - Worldwide Income

b. Estate Taxation - Worldwide Assets

c. Gift Taxation - Worldwide Assets

- Non Resident Alien - Subject to Taxation

a. Income Taxation - United States Source Income, Limited type of Foreign Source Income

b. Estate Tax - United States Situs Assets Only

c. Gift Tax - Real and Tangible Personal Property with a United States Situs

There is a vast difference in the manner in which the United States will apply its income, estate and gift taxes to a would-be immigrant that is considered a "tax resident" and one that still has "non-resident alien" status. A tax resident will be subject to U.S. incomes taxes, estate taxes and gift taxes on a worldwide basis. Non-resident aliens will generally only pay U.S. income tax on income earned from U.S. sources and will pay U.S. estate taxes only on real property and tangible personal property in the United States, and selected intangible assets.

- Resident for Income Tax Purposes

a. Green Card

b. Substantial Presence Test

c. Voluntary Election

d. The Closer Connection Exception

e. Treaties: Tie Breaker

Nonresident Alien

Individuals - Income Tax

A nonresident alien individual is defined as any citizen of a country other than the United States who is not a "U.S. resident" for U.S. income tax purposes. The general rule is that an alien is not considered to be a U.S. resident for tax purposes if the alien does not have (1) a green card representing permanent residency in the U.S. or (2) a "substantial presence or time period" in the U.S. as described below. There are exceptions to this general rule that will also be discussed.

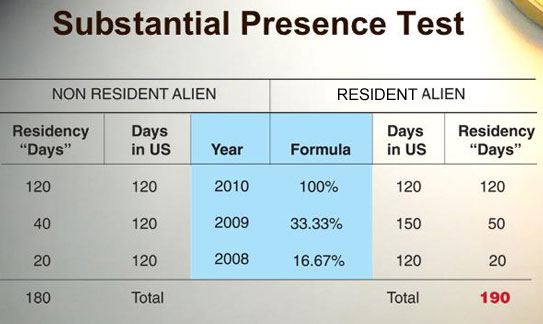

An alien individual has a "substantial presence" in the United States for the calendar year in which the alien is both physically present in the U.S. for at least 31 days and; in that same calendar year is considered to have been in the U.S. for a combined total of 183 days or more over the past three years pursuant to a formula.

For purposes of calculating this combined 3 year, 183-day requirement; each day present in the United States during the current "combined" calendar year counts as a full day, each day in the preceding year as one-third of a day and each day in the second preceding year as one-sixth of a day. This is shown on the example below.

The United States has tax treaties with many countries. These treaties generally provide that the residents and corporations of each country to the treaty are entitled to a more liberal tax treatment than residents and corporations of non-treaty countries. The concept of residency under the treaties is different than the general definition and may permit a nonresident alien to spend more time in the U.S. each year without being a U.S. tax resident. Generally, the tax treaties will permit the alien individual to remain a non-resident for U.S. tax purposes so long as the alien covered by the treaty stays less than 183 days in the U.S. each separate year: and not over the cumulative three year period.

This same type of treatment, that of permitting aliens to have an extended stay in the U.S. of less than 183 days in each year without becoming a U.S. tax resident, is also available to certain aliens that are not from countries governed by a U.S. tax treaty. If an alien has provable close business and social ties to his or her native country; the substantial presence test is extended due to their "closer connection" to a foreign country than to the U.S.

Foreign Corporation - Income Tax

A foreign corporation is a recognized separate taxpayer for U.S. tax purposes. A foreign corporation for U.S. tax purposes, is a corporation that is not organized under the laws of the United States or any one of the states of the United States. A foreign corporation’s articles of incorporation will reflect whether it is a foreign corporation or a U.S. domestic corporation.

III. TWO TYPES OF FEDERAL INCOME TAXATION PATTERNS

U.S. Taxpayers (Citizens and Resident Aliens)

As a general rule, U.S. domestic corporations and United States citizens and residents are taxed by the U.S, on their worldwide net income regardless of the source of the income. Exceptions to this rule exist only to prevent "double taxation" of foreign income earned by U.S. individuals and Companies abroad. Double Taxation is prevented by allowing U.S. taxpayers to obtain a credit against their U.S. tax for foreign taxes paid on that same income.

Foreign Taxpayer

Foreign Taxpayers (both alien individuals and foreign corporations), however, pay U.S. tax on U.S. income in two entirely different ways depending upon whether the income the Foreign Taxpayer earns is from "passive" sources or whether the income results from the Foreign Taxpayer’s conduct of an active trade or business in the U.S.

Furthermore, the U.S. tax rules for Foreign Taxpayers take into account the fact that the jurisdiction of the United States can extend just so far. Therefore, as a general rule a Foreign Taxpayer will only pay U.S. tax on their "U.S. Source Income" and not on income earned from outside of the United States. There are however exceptions.

In order to understand the two different types of taxation, it is important to examine the general rules that define whether a Foreign Taxpayer is conducting an "active business in the U.S." or a "passive investment" as well as the rules governing "source of income" and the "source of deductions". These definitions determine which one of the two sets of tax rules must be applied in order to calculate the U.S. tax liability of foreign corporations and nonresident alien investors.

- Source of Income Rules

a. U.S. Source Income

b. Foreign Source Income

c. Deductions

There are a strict set of rules that govern the determination of whether income finds its source in the United States or a foreign place for U.S. tax purposes. They are as follows:

1. Compensation for personal services. The source of income from the performance of personal services is located at the place where the services are performed.

2. Rents and royalties. Rent or royalty income has its source at the location, or place of use, of the leased or licensed property.

3. Real Property Income and Gain. Income and gain from the rental or sale of real estate has its source at the place where the property is situated.

4. Sale of personal property. Historically, gain from the sale of personal property has been sourced at the "place of sale" which is generally held to be the place where title to the goods passes; however the rules have become more complex taking other factors in place.

5. Interest. The source of interest income is generally determined by reference to the residence of the debtor; interest paid by a resident of the United States constitutes U.S. source income, while interest paid by foreign residents is generally foreign-source income.

6. Dividends. The source of dividend income generally depends on the nationality or place of incorporation of the corporate payor; that is, distributions by U.S. corporations constitute domestic-source income, while dividends of foreign corporations are foreign-source income. There are, however, several important exceptions to these rules.

7. Partially Within and Partially Without. There is a set of source rules that consider the sources of income that can be partially earned in the U.S. and partially from foreign sources such as income from transportation services rendered partly within and partly without the United States; income from the sale of inventory property "produced", "created", "fabricated", "manufactured", "extracted", "preserved", "cured", or "aged" without and sold within the United States or vice versa, and several other types of income. Generally, this is done on some type of allocation basis between the source countries.

Source of Deductions

The source rules for deductions are considerably less specific than those dealing with gross income. The rules regarding claiming deductions against U.S. income earned by a Foreign Taxpayer merely provide that taxable income from domestic or foreign sources is to be determined by properly apportioning or allocating expenses, losses, and other deductions to the items of gross income to which they relate.

- Taxation of Passive (Non Business Income)

a. 30% Flat Tax Rate – Gross Income

b. Withholding obligations

- The Taxation

of Passive Income

If the income that a Foreign Taxpayer earns is passive in nature and does not result from the Foreign Taxpayer conducting an ongoing "trade or business"; the Foreign Taxpayer’s U.S.-source investment income is taxed at a flat 30 percent rate (with no deductions). Generally, the passive types of income earned by investors are such things as interest, dividends, royalties and other periodic payments that arise from the licensing of trademarks, goodwill and numerous types of intellectual property. Foreign Investors that earn only passive U.S. income are also generally not subject to tax on capital gains and other nonrecurring U.S.-source income.

Since as a general rule Foreign Taxpayers earning passive income in the U.S. have only limited ties to the U.S.; a tax "withholding system" is in place. This system essentially forces the U.S. person that is paying the passive income to a Foreign Taxpayer to collect the tax that is due and pay it to the United States. Failure to do so can result in the U.S. person that is responsible to withhold this tax being personally responsible for the tax.

- Taxation of Active Trade or Business Income

a. Graduated Corporate Tax Rates

b. Graduated Individual Tax Rates

c. Effectively Connected Income

Of central importance to the U.S. taxation of Foreign Taxpayers is whether the foreign persons are engaged in a trade or business and, if so, whether the trade or business is located within the United States. Foreign Taxpayers engaged in a trade or business are taxed on their U.S. source income in the same manner as U.S. citizens, tax residents and domestic corporations. That is they are taxed on their taxable U.S. source income after allowable deductions at graduated tax rates.

Whether the Foreign Taxpayer is considered to be engaged in a trade or business within the United States depends on the nature and extent of the taxpayer’s economic contacts with the United States. It is clear that the entire business operation need not be centered in the United States.

The difficult question is, how much of the business functions must be located in the United States in order to create a U.S. trade situs?

A fully integrated enterprise that manufactures and sells its total output in the United States, and is managed and controlled in the United States, is clearly a U.S. trade or business.

At the other end of the spectrum, is the wholly foreign enterprise that merely ships products to customers in the United States, but has no other economic contact with the United States engaged in a U.S. trade or business. Between these two extremes, however, the presence of a U.S. business situs has to be determined on a case-by-case basis, to identify the point at which mere business with the United States crosses the line and becomes business within the United States.

As a general rule, the more deeply a foreign corporation becomes enmeshed in the economic and commercial structure of the United States, the more likely it will be found to have established a trade or business in the United States.

Income Effectively Connected with a U.S. Business

Unlike a Foreign Taxpayer that is taxed on passive U.S. source income only; income of a Foreign Taxpayer that conducts a trade or business in the U.S. will pay tax on all of its United States source income and in limited circumstances, U.S. tax must be paid on income that is earned from foreign sources and not U.S. sources. Foreign source income that is attributable to a

Foreign Taxpayer’s U.S. trade or business activity maybe taxed by the U.S. and is called "Effective Connected Income".

Whether non-U.S. source income earned by a Foreign Taxpayer is taxed as "trade or business" income is determined by how closely the income is attributed to the Foreign Taxpayer’s U.S. trade or business.

In addition to certain foreign source income being subject to U.S. tax; U.S. passive source income may be taxed like trade or business income, if it is considered to be "effectively connected income."

It is possible that at times, U.S. source passive type income will be subject to a tax on net income and not the usual 30% tax that is applied to gross income. For example, though interest income is normally considered "passive income"; it is "active business income" to a Foreign bank that holds deposits and conducts business in the U.S. Therefore, interest earned on such deposits would not be taxed at a flat rate. Rather it is taxed on a progressive rate that permits offsetting deductions for the foreign bank’s cost of funds and other costs of doing business in the U.S.

IV. THE EFFECT OF BILATERAL TREATIES

Bilateral Tax Treaties

The role of bilateral tax treaties in the taxation of Foreign Taxpayers on their U.S. source income is frequently of even greater importance than the basic statutory general rules just mentioned. Tax treaties between the U.S. and other countries can operate to (1) reduce (or even eliminate) the rate of U.S. tax on certain types of U.S. income derived by Foreign Taxpayers situated in the treaty-partner country; (2) override various statutory source of income rules (3) exempt certain types of income or activities from taxation, by one or both treaty-partner countries; and (4) extend credit for taxes levied by one country to situations where the domestic law would not so provide.

The principal purpose of the U.S. bilateral tax treaties is to avoid the potential for double taxation arising from overlapping tax jurisdictions (e.g. income source arising in one country while the taxpayer is resident in the other country.)

The Branch Profits

Tax

There is an additional tax that foreign corporations must be aware of. This is a major trap for the unwary. Absent the tax benefits of an applicable United States tax treaty; a Foreign Corporation may be subject to not only the combined Florida and Federal income tax approaching 40%; but depending upon the facts and circumstances, foreign corporations with earnings from United States investments could be subject to an additional United States tax known as the Branch Profits Tax. The 30% tax is applied to U.S. income that is either not distributed as a dividend or reinvested in U.S. assets by the Foreign Corporation.

Tax Planning Before

Immigrating to the U.S. |

VI. PRE-IMMIGRATION PLANNING – INCOME TAX AND GAINS

- Objective – Minimize United States Gains and Income Tax

a. A nonresident alien, prior to becoming a U.S. tax resident will want to make sure that he or she does not have to pay a U.S. tax on money that as a practical matter, was earned before their residency period.

A key strategy therefore, is to accelerate gains prior to residency so that gains earned while one was a nonresident alien are not subject to U.S. tax after residency is obtained. An example of acceleration would be to trade securities with unrealized gain and sell them before residency. There would be no tax on the gain and the shares can be repurchased with a new high cost basis.

Assume a nonresident alien owned $1.0 million dollars worth of shares of Ford Motor Company that was purchased for $100,000. If the shares are sold after U.S. tax residency is assumed, there will be a tax on $900,000 in gains. A sale of these same shares by a Nonresident before obtaining U.S. income tax residency would result in no taxable gain.

b. Another key strategy is to accelerate income that is expected to be paid after residency. Payments should be collected prior to residency. Examples of income acceleration:1. Exercise stock options

2. Accelerate taxable distributions from deferred compensation plans

3. Accelerate gains on Notes held from installment salesc. One can also defer recognizing a loss until after obtaining residency so that it can be used against post residency gain. Assets with a fair market value below cost can be sold after residency.

VII. Pre Immigration Planning – Estate and Gift Tax

- Residency

for Estate and Gift Tax Purposes

A nonresident alien individual can be subject to the United States estate and gift taxes. However, nonresident aliens are subject to U.S. estate and gift taxes only on assets situated in the U.S.

The definition of nonresidency for estate and gift tax purposes is completely different than the definition of residency for income tax purposes. A nonresident alien for estate and gift tax purposes is an individual whose "domicile" is in a country other than the U.S. Domicile is a subjective test based on one’s intent of permanency in a country. - Objective-Minimize United States Estate Tax

a. Key strategy is to minimize assets in one’s estate before obtaining residency status; and where possible to retain some degree of control over assets.

b. Planned gifts to third parties should be made prior to residency.

c. Planned gifts of United States Situs Property

1. Tangible Property - Physical Change of Situs to a Foreign Situs Before Gift is made.

2. Real Estate - Contribution to foreign corporation and gift of stock in foreign corporation.d. Transfers in Trust for Beneficiaries

VIII. EXCEPTIONAL CIRCUMSTANCES AND SPECIAL TAX BENEFITS

- Students

a. A foreign student who has obtained the proper immigration status will be exempt from being treated as a U.S. resident for U.S. tax purposes even if he or she is here for a substantial time period that would ordinarily result in the student being taxed as a U.S. resident.

b. This student visa not only permits the student to study in the United States but to pay taxes only on income from U.S. sources not worldwide income. The visa also permits the student’s direct relatives to accompany the student to the United States and receive the same tax benefits.

c. Assume the student, a South American woman aged 40, is married to an extremely successful South American businessman who accompanies her with their two children to the U.S. His annual income is $1.0 Million and is earned from the banking business in Columbia. He earns no U.S. income. Under those circumstances, for U.S. income tax purposes, this businessman is exempt from U.S. tax on his worldwide income while living full-time in the U.S. for less than five calendar years.

- Treaty Benefits

a. Aliens that are governed by a tax treaty can generally spend more time in the U.S. than an alien not covered by a treaty before being considered a resident alien for tax purposes.

TAX PLANNING FOR

THE FOREIGN REAL ESTATE INVESTOR |

IX. Real Estate - TAXATION PATTERN

U.S. Taxpayers

- U.S. Citizens, Resident

Aliens and Domestic Corporations

- Real Estate Income Subject to Taxation

a. Income Taxation – Worldwide Income

b. Estate and Gift Taxation (Individuals only) – Worldwide Assets

- Real Estate Income Subject to Taxation

Foreign Taxpayers

- Nonresident Aliens and

Foreign Corporations

- Real Estate Income Subject to Taxation

a. Income Taxation – United States Real Estate Income

- Generally taxed on net income similar to US Taxpayers

- Several Important Exceptions

b. Capital Gains Taxation

- Alien Individual – Individual Tax Rates

- Foreign Corporation – Corporate Tax Rates

c. Estate Taxation

- Alien Individual Residency for Estate Tax Purposes

- U.S. Real Property, U.S companies holding U.S. Real Property and the U.S. estate and gift taxes

d. The Branch Profits Tax (Foreign Corporation Only)

- Real Estate Income Subject to Taxation

Income Tax

Income derived by a Foreign Taxpayer from United States real estate has its own unique taxation pattern that is different in many instances from other types of income earned by the Foreign Taxpayer. A Foreign Taxpayer will generally pay income tax like a United States investor on its real estate income and the Foreign Taxpayer will pay tax on capital gains derived from a sale of United States real property like the U.S. taxpayer.

Capital Gains

Like the U.S. taxpayer, in the event of real estate capital gains, there is a distinct benefit between capital gains earned by a nonresident alien individual who will be taxed at the lower long-term capital gains rate of 15%, and the capital gains earned by a foreign corporation that might carry a Florida state and Federal income tax on the same gain approaching 40%.

Estate/Gift Taxes

A nonresident alien individual can be subject to the United States estate and gift taxes. However, non- resident aliens are subject to U.S. estate and gift taxes only on assets situated in the U.S. U.S. real estate is one of the items that is subject to U.S. estate and gift taxes.

The Branch Tax

There is an additional tax that foreign corporations must be aware of. This is a major trap for the unwary. Subject to the provision of a potentially applicable United States tax treaty; a foreign corporation may be subject to not only the combined Florida and Federal income tax approaching 40%. Foreign corporations with earnings from United States real property investments could be subject the additional United States Branch Tax of 30%.

- How Should the Foreign

Investor Hold U.S. Property – Alien Individual Ownership, Partnerships,

Limited Liability Companies and Foreign and Domestic Corporations

a. Capital Gains Benefits

b. Ordinary Income Taxes

c. Estate Tax Burdens

An alien individual may conduct his or her real estate business in the United States as an individual owner of real property, as a partner in a partnership, as a member of a limited liability company or as a shareholder of a corporation either foreign or domestic.

Individual Ownership and Ownership by Pass

Through Entities

Individual ownership or the use of a limited partnership or limited liability company does generally provide the best income tax results. This is because both partnerships and most (but not all) limited liability companies ("Pass Through Entities") pass all of their U.S. tax attributes to their individual owners directly;as if the entity does not exist for tax purposes. The long-term capital gains rate for a nonresident alien individual will be at a maximum of 15%.

Individual or pass through entity ownership has its income tax benefits but has several drawbacks. The conduct of the real estate business through anything other than the typical corporation will not accomplish the goal of Foreign Investor anonymity.

Ownership individually or through Pass Through Entities require the Foreign Taxpayer Owner to file a U.S. tax return. Furthermore, a nonresident alien’s individual ownership or pass through ownership of U.S. real property will also most likely subject the nonresident alien to a U.S. estate tax on the equity value of the real property. The individual Foreign Taxpayer may at times be forced to trade off the income tax benefit versus these other exposures.

Corporate Ownership

The ordinary income rates and capital gain rates of a corporation are the same. Therefore, both ordinary income and capital gain earned by a corporation can be subject to a U.S. and individual state tax rate approaching 40%; as compared to the 15% capital gain rate paid by a nonresident individual owner.

Furthermore, the payment of dividends by a corporation to its nonresident shareholder might be subject to an additional U.S. withholding tax on dividends. However, ownership of U.S. real property through the corporate form will insure that individual tax returns do not need to be filed by the individual Foreign Investor.

Often with proper tax planning, the tax barriers of corporate ownership of real estate can be significantly reduced.

XI. TAX PLANNING BENEFITS AND TRAPS UNIQUE TO THE FOREIGN INVESTOR IN REAL ESTATE

- Tax Treaties

- Liquidation of Corporation

a. The Problems of Double Taxation

b. Foreign Investors – Payment of a Single U.S. tax

- Portfolio Interest

a. Tax Free U.S. Income

b. U.S. Interest Deductible

c. The Restrictions on Portfolio Interest

d. Planning Techniques

- Sale of Foreign Corporate

Stock

a. Tax Benefits

b. Practical Applications

Once the form of ownership is determined there are several additional planning tools that may be specifically helpful to the Foreign Taxpayer.

Tax Treaties

As mentioned previously, a primary planning tool available to certain Foreign Taxpayer is their ability to rely on a United States tax treaty that may exist with the Foreign Taxpayer’s host country. This type of tax treaty will assure that there is no double taxation between the two countries.

Income will only be taxed at the maximum highest rate of both countries. Treaties may also provide for the prevention of double taxation under the estate tax laws of the two countries, reduce or eliminate the Branch Tax and generally reduce United States taxes on the Foreign Investor’s interest, dividends and business income that are earned from U.S. sources.

A Single U.S. Tax

Even without treaty benefits, Foreign Taxpayers investing in the United States in corporate form can ensure that there will be no dividend or Branch tax on income earned from United States real property by a corporation.

So long as a corporate entity sells or distributes all of its real estate assets and pays a U.S. corporate tax on gain; it may be timely liquidated and distribute all of the sales proceeds free of any further tax. This can avoid a second U.S. tax by the Foreign Taxpayer since the distributions from the Corporation that are liquidation proceeds and not dividends, are excluded from further U.S. taxes.

Portfolio Interest

Another planning tool permits Foreign Taxpayers, both corporate and individual, to benefit from the fact that they are permitted to earn tax-free interest income on certain loans to support U.S. real estate investments. By taking advantage of and meeting the requirements of the "portfolio interest rules", the Foreign Taxpayer may earn tax-free interest instead of taxable real estate profits or dividends.

Sale of Stock/Foreign

Corporation

U.S. taxes on real estate profits can be totally eliminated in rare occasions in which a real estate buyer is willing to acquire a Foreign Taxpayer’s shares in a foreign corporation that owns U.S. real estate. A Foreign Taxpayer may form a foreign corporation to own United States real estate. Gain from the sale of shares of stock in that foreign corporation by the Foreign Taxpayer generally is not subject to tax; even if the foreign corporation owns U.S. real estate. Due to its many complexities, this technique is applicable only in very limited situations and is not considered to any degree in this outline.

XII. THE TAX PLANNING STRUCTURES

- Specific Tax Planning

Entities for Nonresident Aliens and Foreign Corporate Real Estate Investors

- Objective – Minimize

U.S. Income Tax, Capital Gains and Estate Tax on Real Estate Profits. It is

important to note that income tax planning and estate and gift tax planning

are often at cross purposes.

- The Structure –

Individual or Partnership or Limited Liability Company Ownership

a. Income Tax

b. Capital Gains Tax

c. Estate Tax

- The Structure –

Foreign Corporation Ownership

a. Income Tax

b. Estate Tax

c. Branch Tax

- The Structure –

A Foreign Holding Company and a U.S. Subsidiary

a. Income Tax

b. Estate Tax

c. Branch Tax

To take advantage of any of the several unique tax benefits and avoid the traps, the Taxpayer Investor must find the proper investment vehicle that meets the Foreign Taxpayer’s tax needs and his or her other personal and commercial needs. Each Foreign Taxpayer will find that their tax structure will be unique to them and the various tax planning techniques fit in some situations and not others.

There are three very basic structures that will show the different types of tax considerations depending upon the nature of the real estate. A chart of the three structures and their tax attributes may be found following this discussion. The cost factor of any tax planning structure must be considered in advance. Generally, a transaction should be of a certain significant size to benefit from the more complex structures.

Individual Ownership/Pass

Through Entity

Individual ownership of real property by a nonresident alien or ownership through a Pass Through Entity results in the nonresident alien being required to file a U.S. tax return and most likely subjects him or her to estate taxes on the real property. However, it is the best vehicle for income tax purposes.

Foreign Corporate

Ownership

A Foreign Taxpayer investing in passive real estate (that is not income producing, such as raw land) who wishes to avoid estate taxes and preserve anonymity might use a single foreign corporation to own the real estate.

The Foreign Taxpayer should know that the capital gains earned by the foreign corporation from the sale of the real estate could be significantly higher than individual ownership. Since there is no annual income from passive real estate holdings, the Branch Tax can be avoided by the liquidation of the foreign corporation after the sale of the foreign corporation’s real estate.

Real Estate Holding

Company

A Foreign Taxpayer involved in the active real estate business, such as ownership of income producing property or development property, may as a general rule, invest in the following fashion. The Foreign Taxpayer will form a foreign holding corporation that then is the 100% owner of a domestic corporation such as a Florida corporation. The Florida corporation is the direct real estate owner.

This structure can eliminate at least two of the three taxes that the Foreign Taxpayer might face. Since the direct investor in the real estate is a domestic corporation, it need not pay any Branch tax on its profits. Since the Foreign Investor owns only shares in a foreign corporation, there is no estate tax upon his or her demise. The income tax, however, is generally unfavorable as compared to individual ownership.

# # #

Copyright © 2004-2014

This firm has had extensive experience with all areas of the Internal Revenue Code that apply to both non-resident aliens and foreign corporations investing or conducting business in the United States, and U.S. citizens and domestic corporations investing abroad.

Richard S. Lehman, Esq.

-

Georgetown University J.D.

Georgetown University J.D. - New York University L.L.M. Tax

- Law Clerk to the Honorable William M. Fay - U.S. Tax Court

- Senior Attorney, Interpretive Division, Chief Counsel’s office, Internal Revenue Service

- Author: “Federal Estate Taxation of Non-Resident Aliens,” Florida Bar Journal

- Contributing Author and Editor: International Business and Investment Opportunities” Florida Department of Commerce, Division of Economic Development, Bureau of International Development (translated in German, Spanish, and Japanese)

Today’s tax and financial planning landscape is a complex one, undergoing constant change. If businesses and individuals expect to make the proper moves, keep abreast of changing legislation, and make sure that they legally pay the least amount of taxes, they must rely on tax attorneys.

Richard S. Lehman has been meeting these needs when it comes to dealing with the federal tax law for more than three decades. Thanks to a team of tax attorneys who are familiar with every aspect of the Internal Revenue Code, the tax needs of international and domestic clients, corporations and individuals have been met. The firm has been involved in unique and complex tax situations on behalf of the affluent from its beginning.

Richard S. Lehman, with four years of U.S. Tax Court and Internal Revenue Service experience in Washington D.C., has built a boutique tax law firm with a national reputation for being able to handle the toughest tax cases, structure the most sophisticated income tax and estate tax plans, and defend clients before the Internal Revenue Service. It regularly works with law firms, accountants, businesses and individuals struggling to find their way through the complexities of the tax law. In short, the firm is a valuable resource to each of these audiences.

Central to the firm’s philosophy is the recognition that the tax laws do not exist in a vacuum. Legal and other professional disciplines often need to be woven together to assure a successful outcome. Consequently, the firm is regularly approached by and often works with the finest professionals in many areas of the law and the business world to untangle complex tax situations that require its specialized expertise.

Regardless of the issue, the firm has consistently guided clients on topics ranging from complex tax scenarios in real estate, business acquisitions and sales, securities offerings, tax contests, probate litigation and numerous other areas of commerce.

Mr. Lehman assures each client of his personal attention at all times.

Richard S. Lehman, Esq

Lehman Tax Law

Located in the Dorot & Bensimon P.L. Domestic & International Tax Law Office

2000 Glades Road, Suite 312

Boca Raton, FL. 33431

- Tel: 561-368-1113

- Fax: 561-981-8203

- Skype: LehmanTaxLaw

- Email: rlehman@lehmantaxlaw.com

International Attorney Website: www.LehmanTaxLaw.nl

New IRS Streamlined Compliance Procedure

In the 30 minute video below, the new I.R.S. changes to Offshore Bank And Foreign Asset Disclosure Programs is explained by United States Tax Attorney, Richard S. Lehman. This is an extremely important and valuable I.R.S. Program. It allows almost every American who has been afraid to step forward and disclose their foreign assets to the U.S. taxing authorities to do so with minimized penalties on unpaid taxes and unfiled information returns.

Taxation of the Clawback in a Ponzi Scheme - Maximum Tax Recovery

The taxpayer must also learn about what is called the “mitigation section”. This is internal revenue code section 1341 that permits one type of the Clawback payment to be taken as an ordinary income deduction in the year in which the Clawback income was originally taxed even if the year is closed by the statute of limitations; while another type of clawback payment may be deductible only in the year of payment.